Tax Implications on Forex Transactions – TCS on remittances outside India

Forex Transactions refer to transferring funds from one country to another. There could be various personal as well as business-related reasons due to which funds are required to be remitted abroad.

But have you ever wondered what the

tax implications on Forex transactions are? What is the mechanism for paying tax on Forex transactions? Heard about Liberalized Remittance Scheme but don't know what exactly it is?

Let's walk through this article to get the answers to all these questions –

Liberalized Remittance Scheme (LRS)

Under the LRS scheme, a resident person can remit outside India funds up to US$ 2,50,000 without prior permission of Reserve Bank of India for the financial year April 1 to March 31. This scheme is available only for Individuals (including minors) and not for corporates, LLPs, partnership firms, HUF, etc.

Transactions that an Individual can engage in under Liberalized Remittance Scheme (LRS)

A resident Individual is allowed to engage in any Current or Capital account transaction or a blend of both.

Permissible

capital account transaction comprises of buying of property abroad, opening foreign currency account overseas with a bank, investing in shares by acquiring listed and unlisted stocks, lending loans to NRI, and setting up a wholly-owned subsidiary or a joint venture governed by the provisions placed by the Foreign Exchange Management Act.

Permissible

current account transaction involves private visit, grants, going overseas for employment or emigration purposes or for taking care of relatives, business purposes, medical purposes, studies, facility to grant loan in rupee to non-resident individual or person of Indian origin and close relatives under the scheme and other current account transactions allowable under the FEMA act.

Tax Implications on Forex Transactions

- As per section 206C (1G) of the Income-tax Act, 1961, Forex transactions are liable to tax if the amount exceeds a specific limit. The limits are subject to variation from time to time.

- The existing rules have got effective from October 1, 2020, as per the Finance bill, 2020. According to the provisions of the Income-tax Act, an amount of up to Rs. 7 lakhs per financial year is exempt from tax liability.

- Amount exceeding Rs. 7 lakhs would be liable to tax. On such an amount, tax has to be paid on TCS (Tax Collected at Source) basis.

- In the case of international tour packages, Travel Company would collect TCS irrespective of the package cost, and the TCS would be applicable to individuals on the entire amount of payments. The threshold limit of Rs. 7,00,000 is not applicable in this case.

- Currently, the tax rate applicable on payment over and above Rs. 7 lakhs is 5%, and for education loan transactions, it is 0.5%.

- In case of non-availability of Permanent Account Number of the individual, TCS is applicable at 10%.

- In some instances, GST is leviable for currency conversion and on remittance charges. Such GST charges are not considered for making TCS collection.

- In order to claim a refund on account of such tax collected at source or to adjust it with overall tax liability, the individual has to file his Income Tax return within prescribed due dates.

Let's have a look at few examples to have a better understanding of the provisions mentioned above:

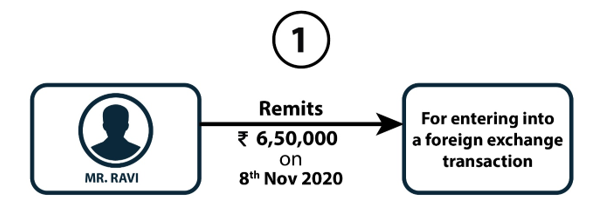

Taxability:

Taxability:

Since the transaction amount is less than Rs. 7,00,000, tax would not be applicable on such amount.

Taxability:

In this case, TCS would be collected on the amount exceeding Rs. 7,00,000 at the rate of 5%.

- Tax amount = 5% of Rs. 4,00,000 (Rs. 11,00,000-Rs. 7,00,000) = Rs. 20,000

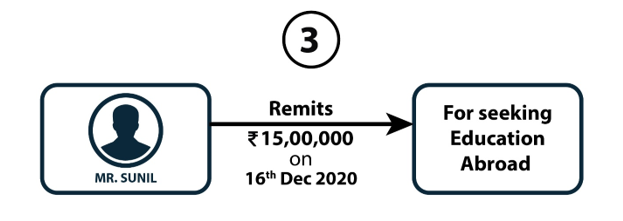

Taxability:

Taxability:

Since the payment has been made for pursuing studies, the tax rate applicable would be 0.5%.

- Tax amount = 0.5% of Rs. 8,00,000 (Rs. 15,00,000-Rs. 7,00,000) = Rs. 4000

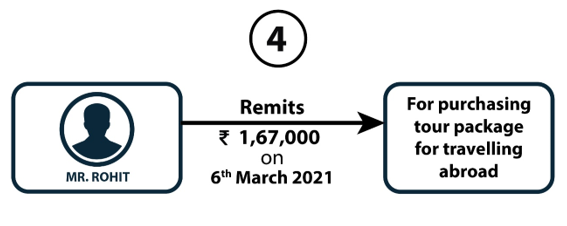

Taxability:

Since the payment has been made for purchasing tour package, no threshold limit would applicable for collecting tax on such amount. Hence, tax would be calculated on the entire sum of Rs. 1,67,000 at rate of 5%.

- Tax amount = 5% of Rs. 1,67,000 = Rs. 8350

Summing-up:

- The resident individuals can freely enter into a transaction of up to USD 2,50,000 under the Liberalized Remittance Scheme of Reserve Bank of India for a particular financial year from 1st April to 31st March.

- A resident individual can enter into Current and Capital account transactions or a blend of both these kinds of transactions prescribed by the Reserve Bank of India as per the guidelines of the Foreign Exchange Management Act.

- W.e.f. October 1, 2020, foreign exchange transactions of up to Rs. 7,00,000 in a financial year are free from tax liability. Amount exceeding Rs. 7,00,000 is liable to TCS (Tax collected at Source) in the hands of the individual at 5% and 0.5% in case of education loan transaction.

- Individuals can claim tax refund or adjust the tax collected with overall tax liability by filing the Income Tax return.

- For tour packages, there is no minimum threshold limit for collecting tax.

Authored by

CA Manish Gupta and assisted by

Kriti Agrawal

For any queries, kindly contact at

info@manishanilgupta.com

0 Comment